Burke & Schindler

Burke & Schindler Pro • tem legal solutons

Pro • tem legal solutons Burke Pros

Burke Pros Concentric Wealth Management

Concentric Wealth Management

The first quarter of 2026 reminded investors how easy it is to get lost in the trees. The year began with a constructive backdrop: economic growth was positive, inflation was moderating, corporate earnings expectations were supportive, and central banks were moving gradually toward easier policy. That changed abruptly late in the quarter as geopolitical conflict in the Middle East sent energy prices higher and forced markets to reassess the outlook for inflation, interest rates, and growth.

Still, seeing the forest through the trees requires stepping back from the immediate disruption and focusing on the broader landscape. The U.S. economy entered this period from a position of relative resilience as growth outside the conflict zone has not broken down and several long-term drivers such Business investment and productivity-enhancing technology spending remain intact. In the second quarter, markets are likely to be shaped by the balance between these underlying strengths and the pressures of higher energy costs, tighter financial conditions, and elevated geopolitical risk.

Q1 Market Review

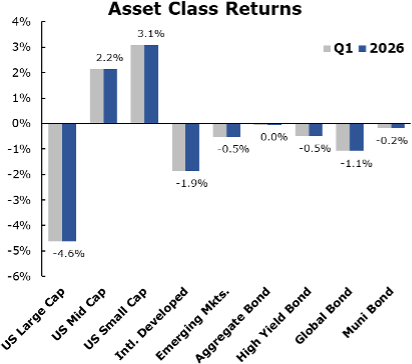

The first quarter was defined by the late-February escalation in the Middle East, which quickly drove oil and gasoline prices higher and rippled across global markets. The S&P 500 declined 4%, Treasury yields moved modestly higher as inflation expectations rose, and credit spreads widened.

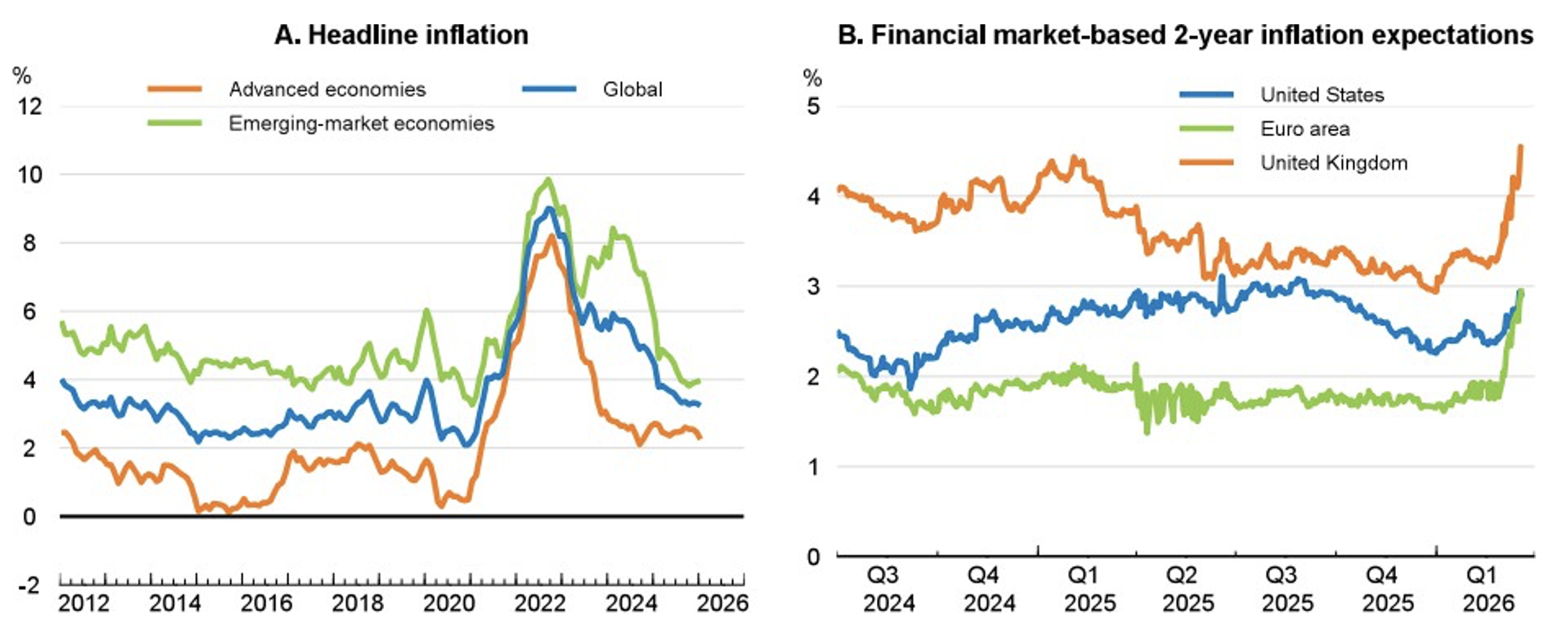

Even before the geopolitical shock, the U.S. economy was showing signs of cooling. Growth had slowed, payroll gains had weakened, unemployment edged up to 4.4%, and consumer spending was still positive but losing momentum. Inflation had been trending lower, but the energy shock complicated that progress and reinforced a more cautious stance from the Federal Reserve.

Market leadership also shifted. Energy and materials outperformed, while parts of technology came under pressure as investors became more selective about AI’s potential effects on business models and margins. At the same time, market breadth improved, with leadership beginning to extend beyond a narrow group of mega-cap stocks.

Economic Outlook

Growth in the second quarter may be slower, but still positive. Higher energy prices act like a tax on consumers and businesses by raising inflation while pressuring margins and purchasing power. The U.S. tends to be more insulated than many other regions because it is a net energy producer, and the broader economy entered the year with healthier fundamentals than many expected. Consensus estimates suggest the oil shock could add to headline inflation while subtracting modestly from GDP, rather than pushing the economy directly into recession.

The key variable is duration. If energy prices stabilize and the conflict de-escalates, the economic damage could remain contained. If the conflict persists or intensifies, the mix becomes more stagflationary: inflation stays firmer while growth slows further. In the U.S., business investment and AI-related capital spending remain important offsets. Abroad, the picture is more uneven, as Europe and the UK appear more vulnerable due to their greater dependence on imported energy. Japan still has supportive domestic policy and corporate investment trends. China faces a different challenge: softer domestic demand and ongoing pressure in property and consumption, even if it is somewhat less exposed to the direct energy shock than Europe.

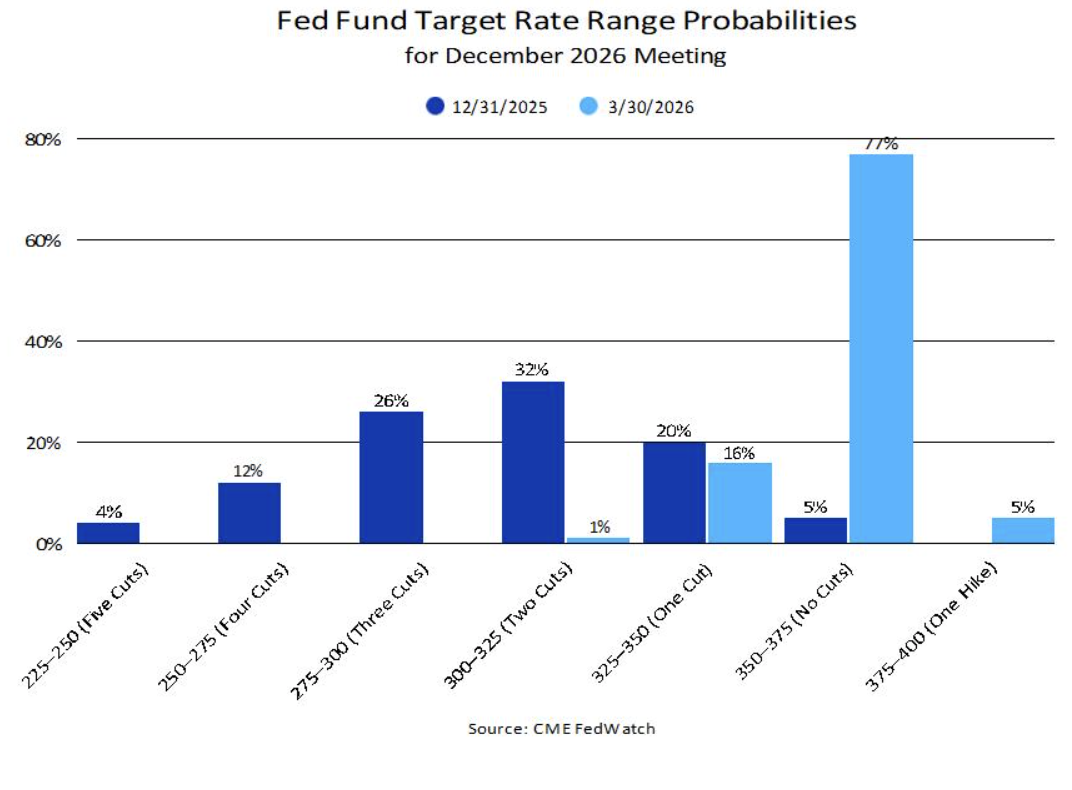

Central banks are facing a difficult balancing act. In the U.S., the policy debate has shifted from when rate cuts will occur to whether inflation pressure from commodities delays them meaningfully. Europe may face even more pressure because inflation sensitivity there is higher and energy dependence is greater. Policy is likely to remain highly data dependent, but the path to easier monetary conditions is less straightforward than it appeared at the start of the year.

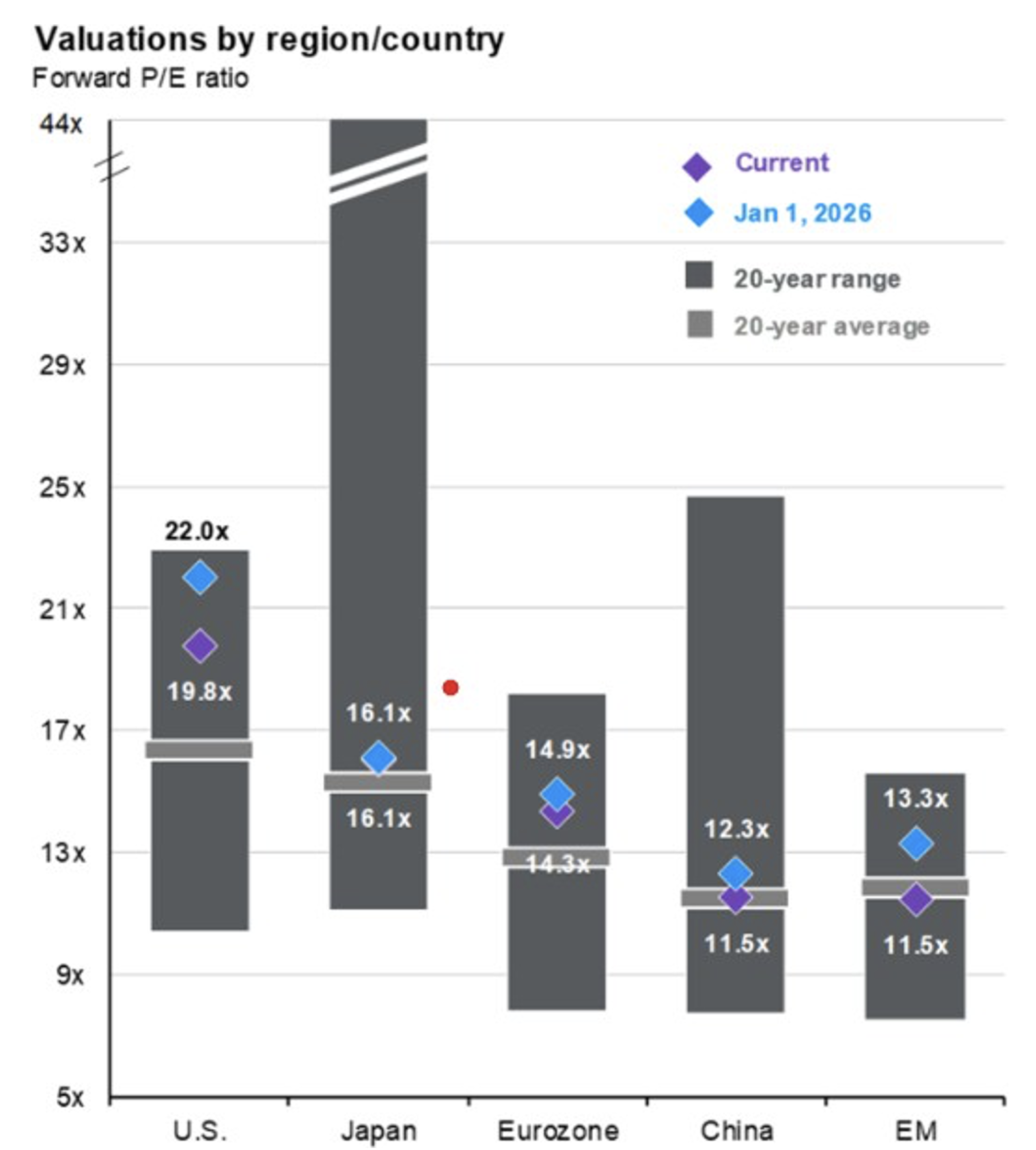

Equity Markets

Source: JPMorgan Guide to the Markets

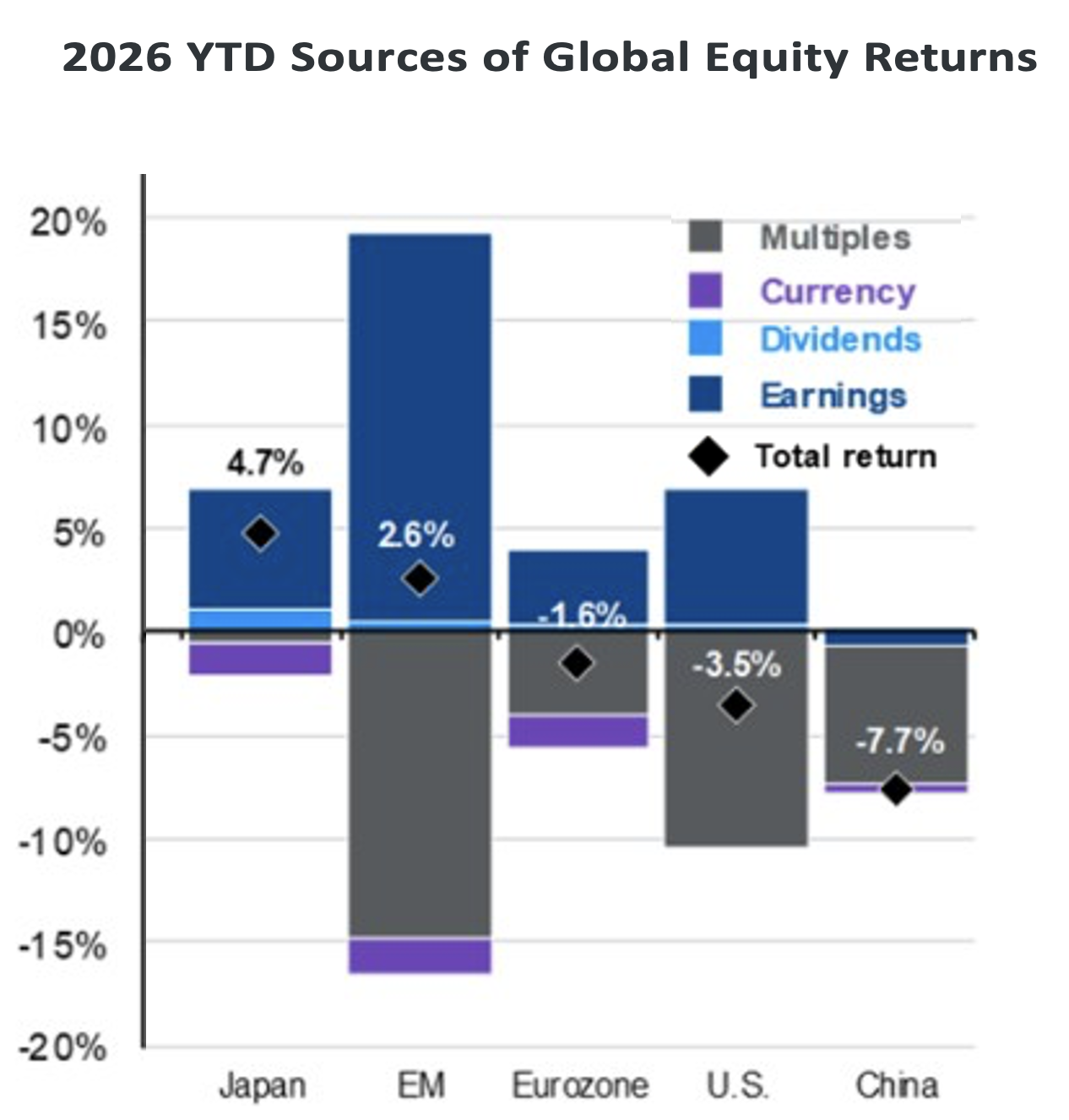

For domestic equities, earnings remain the central support. The market is likely to remain volatile, but the fundamental story is improving beneath the surface. U.S. earnings growth is broadening beyond the largest AI-linked companies and more sectors are participating than in the prior several years. In our view, value-oriented shares, dividend-paying companies, and businesses tied to the next phase of AI investment may be better positioned in a market that is demanding more discipline and less willing to reward every growth story equally.

Source: JPMorgan Guide to the Markets

The main near-term risk for U.S. equities is, again, that higher commodity prices start to compress margins and weaken demand more materially. If that happens, leadership could narrow again toward businesses with stronger pricing power and steadier earnings. If energy markets calm, however, earnings should regain prominence and the case for a broader advance improves.

Internationally, opportunity exists, but selectivity matters. Europe and Japan still offer more attractive valuations than much of the U.S. market, and Japan in particular has supportive policy and corporate investment trends. Emerging markets are bifurcated. Commodity exporters have been beneficiaries of the recent move, while import-dependent

have faced greater pressure from higher energy costs.

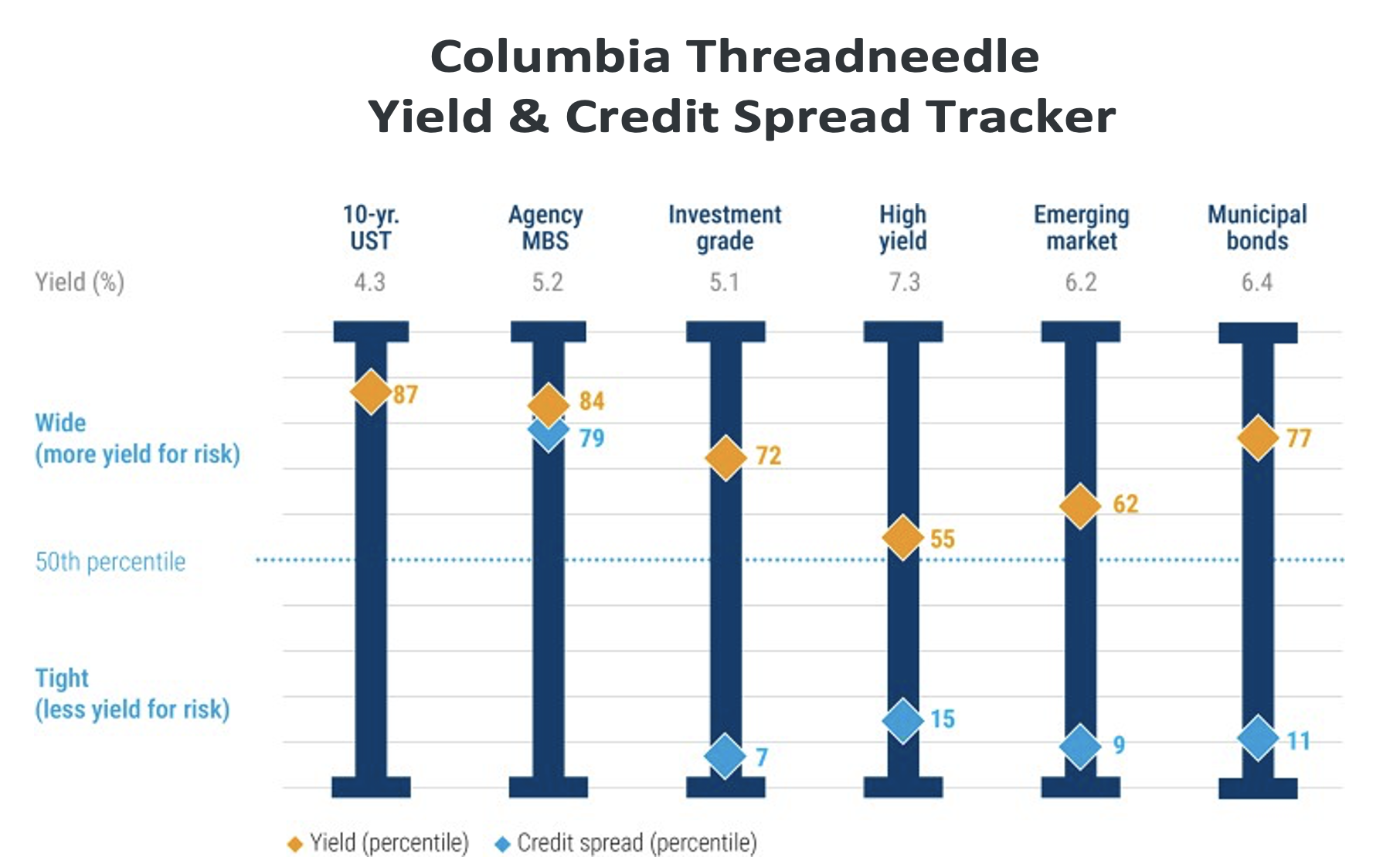

Fixed Income Markets

The bond market is balancing two competing forces: higher near-term inflation from energy and the possibility of slower growth later on. Treasury yields moved higher during the first quarter as investors priced in inflation risk and a less certain rate path, but if growth slows more noticeably as the year progresses, high-quality bonds should again provide ballast. Several of the materials point to long-end yields staying relatively elevated because of fiscal deficits and elevated term premium, even if policy rates ultimately move lower.

Within credit, fundamentals remain decent, but spreads aren’t as generous in many areas. That makes broad exposure less compelling than selective exposure. Areas offering income with better structural support appear more attractive than certain crowded segments. Municipal bonds, senior loans, preferred securities, and certain forms of private credit remain areas where we see relative opportunity. Municipal bonds have been supported by favorable technicals, healthy state and local fundamentals, and relatively attractive yields.

Real Assets & Alternative Investments

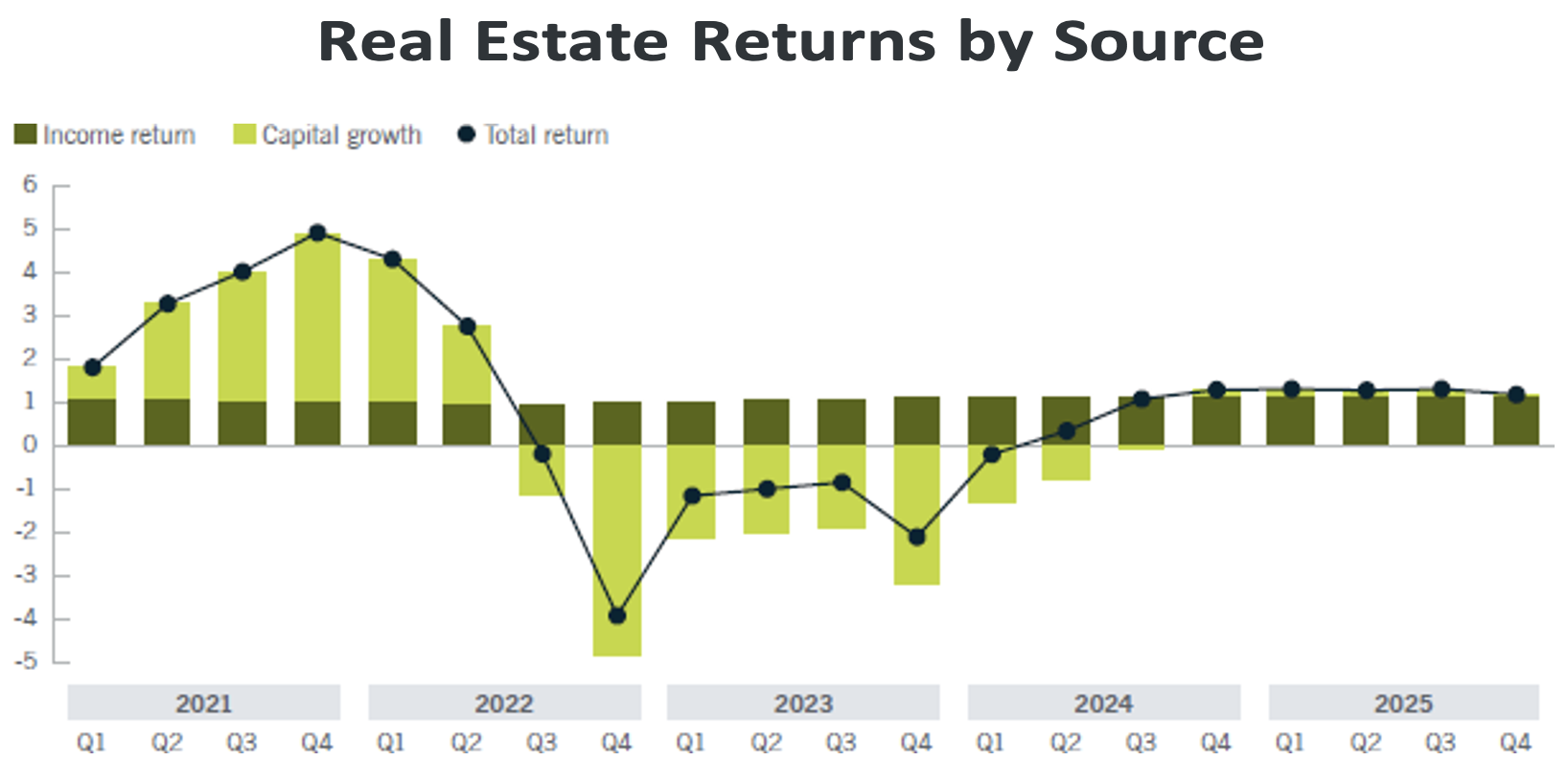

Real assets had a mixed first quarter, but the backdrop for the category remains constructive. Energy-related assets benefited from the commodity shock, while gold, after a powerful run, turned volatile as some holders raised liquidity. More broadly, real assets continue to offer an important combination of diversification, inflation sensitivity, and exposure to long-duration structural themes.

Looking ahead, infrastructure remains one of the more compelling areas within alternatives. Rising power demand, digital buildout, energy storage, transmission needs, and data-center expansion all point to a durable pipeline of opportunity. Private real estate also appears to be in a recovery phase, with improving income returns, reduced new supply, and better conditions in select sectors such as industrial, housing-related segments, senior housing, and data centers. These are not broad, one-size-fits-all opportunities; rather, they are increasingly theme-specific.

Within broader alternatives, private credit and selective private equity still look attractive where underwriting standards are strong and capital is being deployed carefully. The common thread across alternatives is selectivity: in a market where many traditional assets already reflect a good deal of optimism, differentiated exposures tied to real cash flows, infrastructure needs, and disciplined credit creation may offer more durable return potential.

Summary: The Path Ahead

As we enter the second quarter, investors are navigating a market shaped by uncertainty, but not without opportunity. The immediate questions around inflation, energy prices, and geopolitical risk are important, but they are not the whole story. Seeing the forest through the trees means looking beyond the headlines and keeping sight of the broader investment landscape: an economy that remains resilient, a market that is beginning to broaden, and long-term opportunities still rooted in quality, income, and structural growth.

Our view is that this environment calls for perspective over prediction and discipline over reaction. Well-diversified portfolios, grounded in resilient earnings, dependable income, and selective exposure to long-term themes, remain the best way to navigate periods like this. Volatility may remain with us in the near term, but for patient investors, it can also create opportunity. In that sense, the task is not to lose sight of the forest because of the trees, but to use the trees to better understand the forest ahead.

Disclosures

Asset allocation does not assure or guarantee better performance and cannot eliminate the risk of investment losses. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on Concentric Wealth Management research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss. All investing involves risk including loss of principal. No strategy assures success or protects against loss There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk. Rebalancing a portfolio may cause investors to incur tax liabilities and/or transaction costs and does not assure a profit or protect against a loss. The fast price swings in commodities will result in significant volatility in an investor’s holdings. Commodities include increased risks, such as political, economic, and currency instability, and may not be suitable for all investors.

When referencing asset class returns or statistics, the following indices are used to represent those asset classes, unless otherwise noted. Each index is unmanaged, and investors can not actually invest directly into an index:

US Large Cap – S&P 500 Total Return

- US Mid Cap – S&P 400 Total Return

US Small Cap – S&P 600 Total Return

International Developed – MSCI EAFE Total Return

Emerging Markets – MSCI Emerging Markets Total Return

- Aggregate Bond – Bloomberg US Aggregate

- High Yield Bond – Bloomberg US Corporate High Yield

- Global Bond – Bloomberg Global Aggregate

- Municipal Bond – Bloomberg Municipal Bond

Domestic Equity can be volatile. The rise or fall in prices take place for a number of reasons including, but not limited to changes to underlying company conditions. International Equity can be volatile. The rise or fall in prices take place for a number of reasons including, but not limited to changes to underlying company conditions. Fixed Income securities are subject to interest rate risks, the risk of default and liquidity risk. U.S. investors exposed to non-U.S. fixed income may also be subject to currency risk and fluctuations. Cash may be subject to the loss of principal and over a longer period of time may lose purchasing power due to inflation sector or industry factors, or other macro events. These may happen quickly and unpredictably. International equity allocations may also be impacted by currency and/or country specific risks which may result in lower liquidity in some markets. Marketable Alternatives involves higher risk and is suitable only for sophisticated investors. Along with traditional market risks, marketable alternatives are also subject to higher fees, lower liquidity and the potential for leverage that may amplify volatility or the potential for loss of capital. Additionally, short selling involved certain risks including, but not limited to additional costs, and the potential for unlimited loss on certain short sale positions.

S&P Total Return 500 – Covers the 500 largest companies that are in the United States. These companies can vary across various sectors.

S&P MidCap 400 Total Return Index– A stock market index from S&P Dow Jones Indices. The index serves as a barometer for the U.S. mid-cap equities sector and is the most widely followed mid-cap index.

S&P SmallCap Total Return 600 – Seeks to measure the small-cap segment of the U.S. equity market. The index is designed to track companies that meet specific inclusion criteria to ensure that they are liquid and financially viable.

MSCI EAFE Total Return Index – An equity index which captures large and mid cap representation across 21 Developed Markets countries* around the world, excluding the US and Canada. The index covers approximately 85% of the free float adjusted market capitalization in each country.

MSCI Emerging Markets Total Return Index – Captures large and mid cap representation across 25 Emerging Markets (EM) countries. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

Bloomberg US Aggregate Bond Total Return Index – Used as a benchmark for investment grade bonds within the United States.

Bloomberg US Corporate High Yield Total Return Index – Covers performance for United States high yield corporate bonds. This index serves as an important benchmark for portfolios that include exposure to riskier corporate bonds that might not necessarily be investment grade.

Bloomberg Global Aggregate Total Return Index – Measures the performance of global investment grade fixed income securities. This index is widely used as a benchmark for fixed income securities.

Bloomberg Municipal Total Return Index – Serves as a benchmark for the US municipal bond market.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost. Indexes discussed are unmanaged and you cannot directly invest into an index. Past performance is not a guarantee of future results.

Securities and advisory services offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC