Burke & Schindler

Burke & Schindler Pro • tem legal solutons

Pro • tem legal solutons Burke Pros

Burke Pros Concentric Wealth Management

Concentric Wealth Management

Prelude

The First Quarter of 2024 was marked by a continued rally in equities and continued softness in bond prices, though yields trudged higher. The economic backdrop continued to be mixed as leading indicators continued to be tight while lagging indicators continue to flag a nearly an all-clear signal. We see risks stemming from sticky inflation, monetary policy, and the uncertain direction of the rate environment causing pressure on equity markets.

Economics

Source: Concentric Wealth Global Macro Regime Indicator

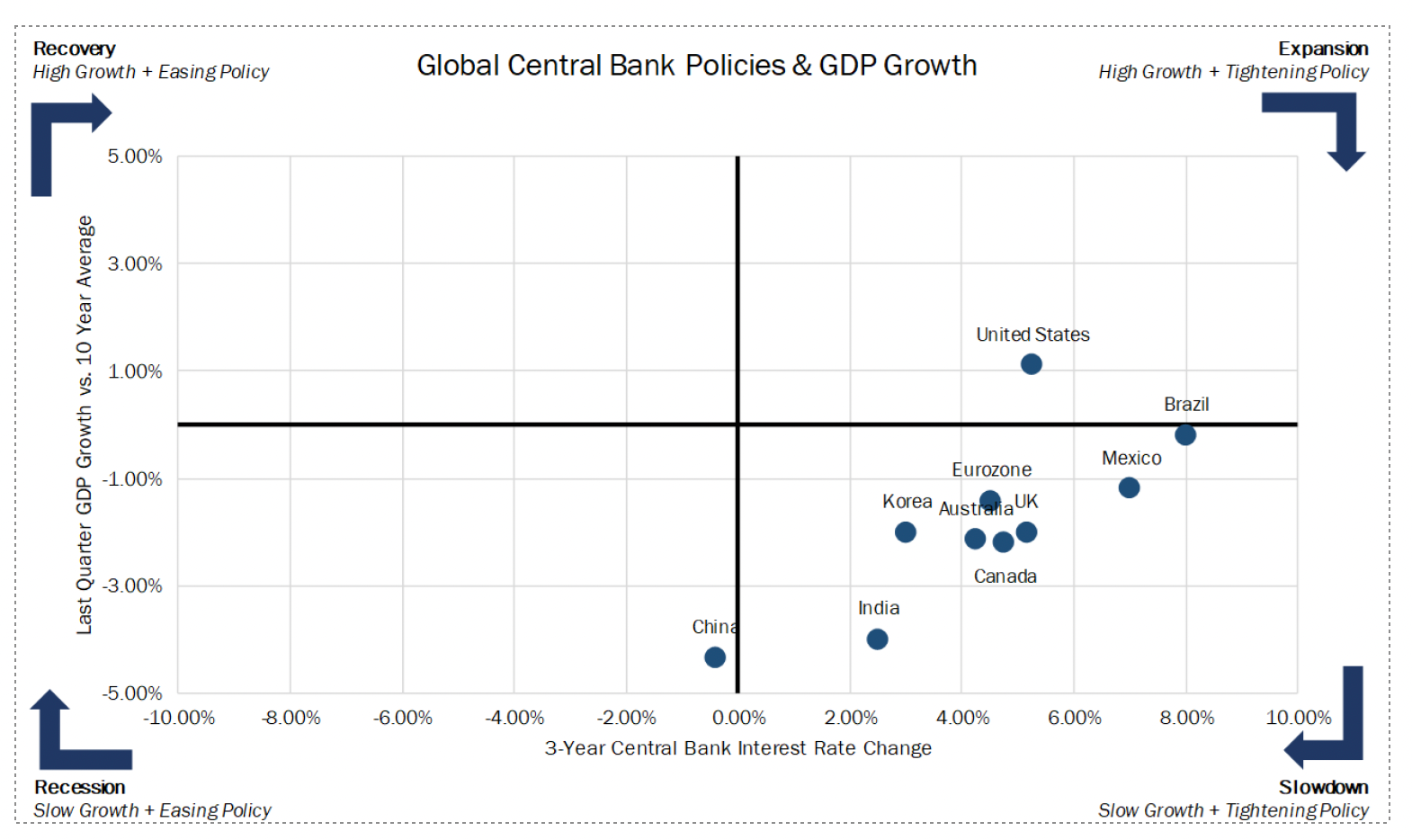

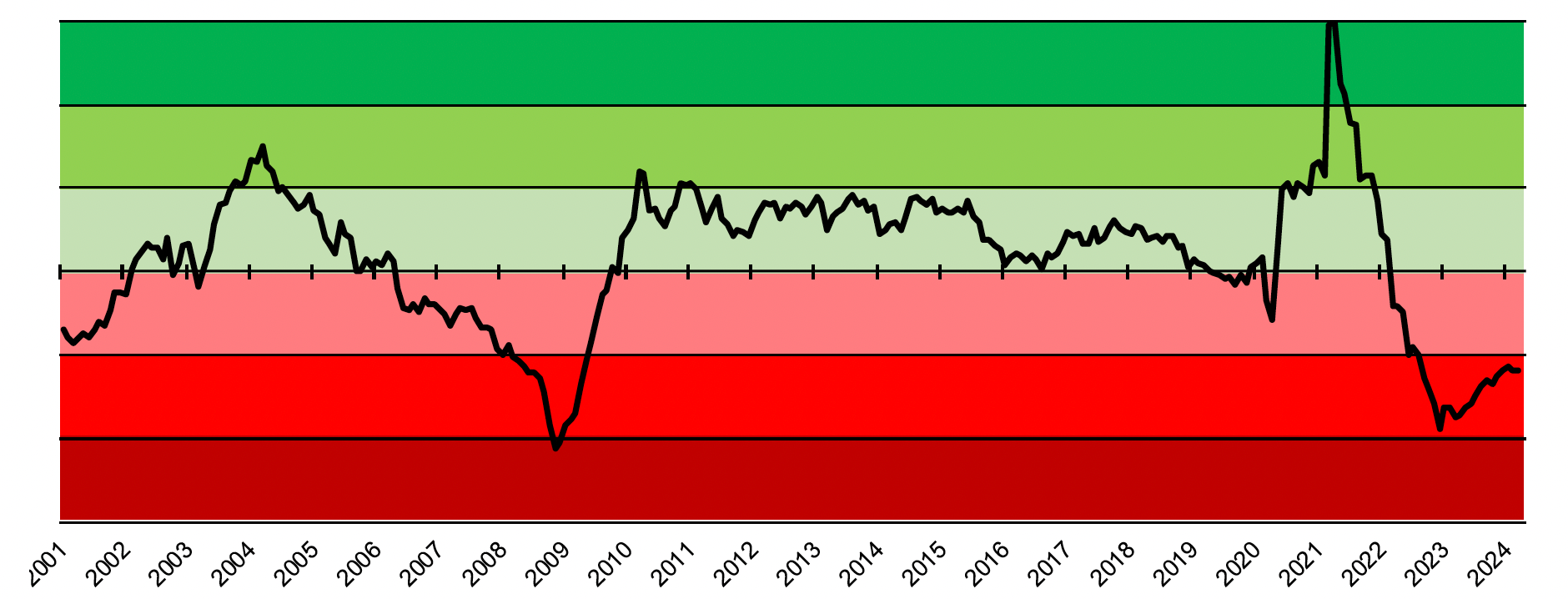

The global economy continues to show late-cycle conditions as quarter-over-quarter gross domestic product (GDP) growth continues to be below the longer-term average paired with high interest rates from global central banks. The United States appears to be more resilient to high rates as the consumer, who drives roughly 70% of GDP growth or decline, continues to be relatively well capitalized and able to absorb a combination of continued high rates and heightened inflation. Notably, Eurozone economies are seeing slowing economic growth and China continues to struggle with a mix of a weak real estate sector and depressed consumer confidence. In the United States, leading economic indicators continues to be weak while lagging economic indicators are showing signs of improvement. We see risks stemming from the potential for a slowdown in job growth as well as cost fatigue from the United States consumer, which could tip us into a mild recession. All the while, if inflation continues to subside and job growth remains steady with real wage inflation, the U.S. Federal Reserve (the Fed) could have the soft-landing that it is touting. Inflation remaining sticky, which is a key metric for the Fed and has been since 2022, could keep rates higher for longer leading to a potential delay in an easing cycle resulting in likely recessionary conditions.

Economic Conditions Indicator Since 2001

Source: Concentric Wealth United States Macro Regime Indicator

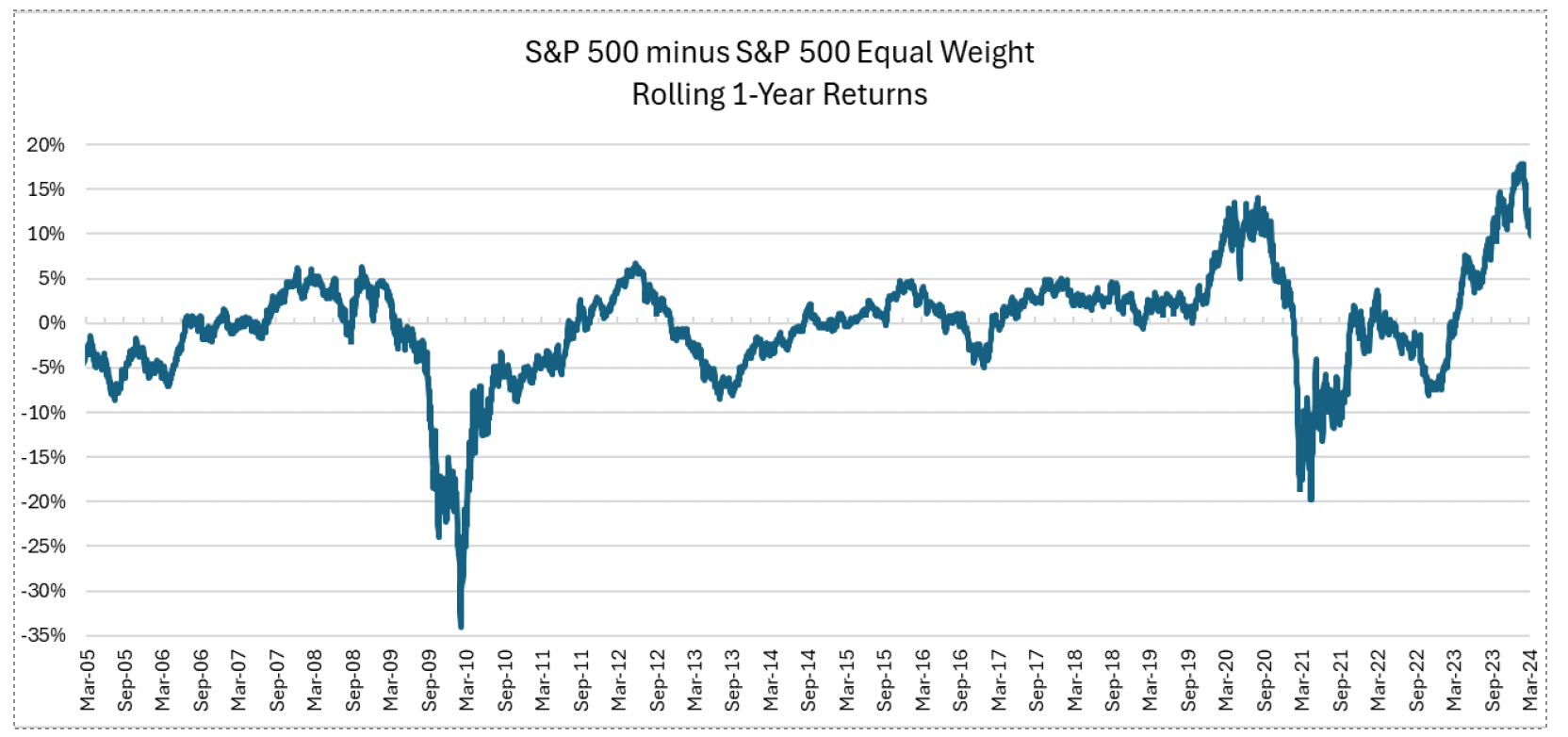

Market Concentration Evening Out

Source: YCharts, The London Company

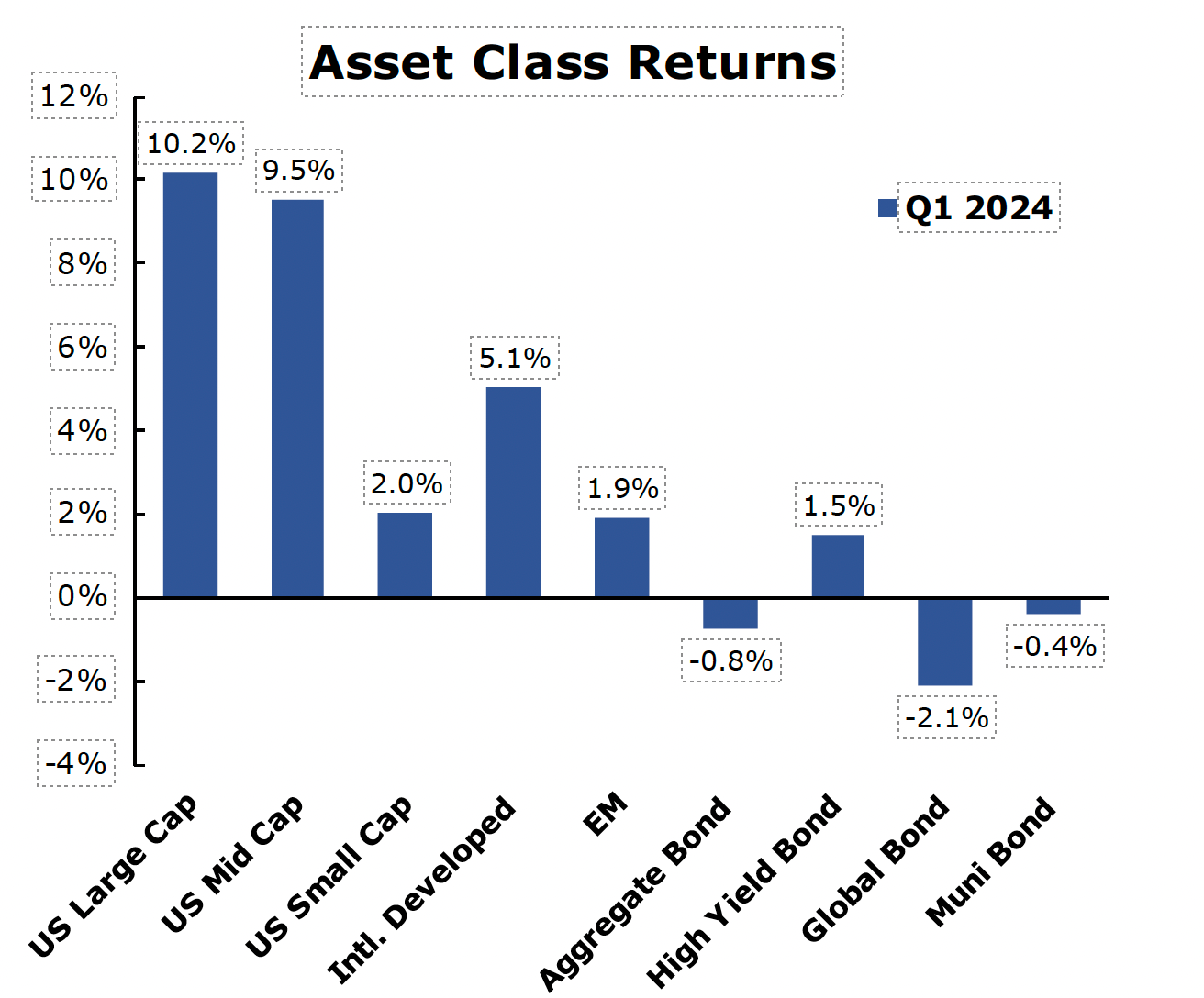

The first quarter of 2024 was a strong start to the year with many trends that emerged late in 2023 persisting. Gains in domestic markets continued to be driven by the largest names in the S&P 500 with the top 9 names contributing 75% of the gains in Q1 2024. We are starting to see signs of broadening market performance as evidenced by the equal weight S&P 500 index showing improved performance relative to the S&P 500. Artificial intelligence is a theme that has continued to dominate headlines with an outsized impact on equity prices and valuations as investors assess what levels of productivity, health, and innovation the technology can drive. We view the AI theme with caution as, with any disruptive technology, it has the potential to drive bubble-like valuations as well as the potential for scrutiny by regulators attempting to define and oversee the technology.

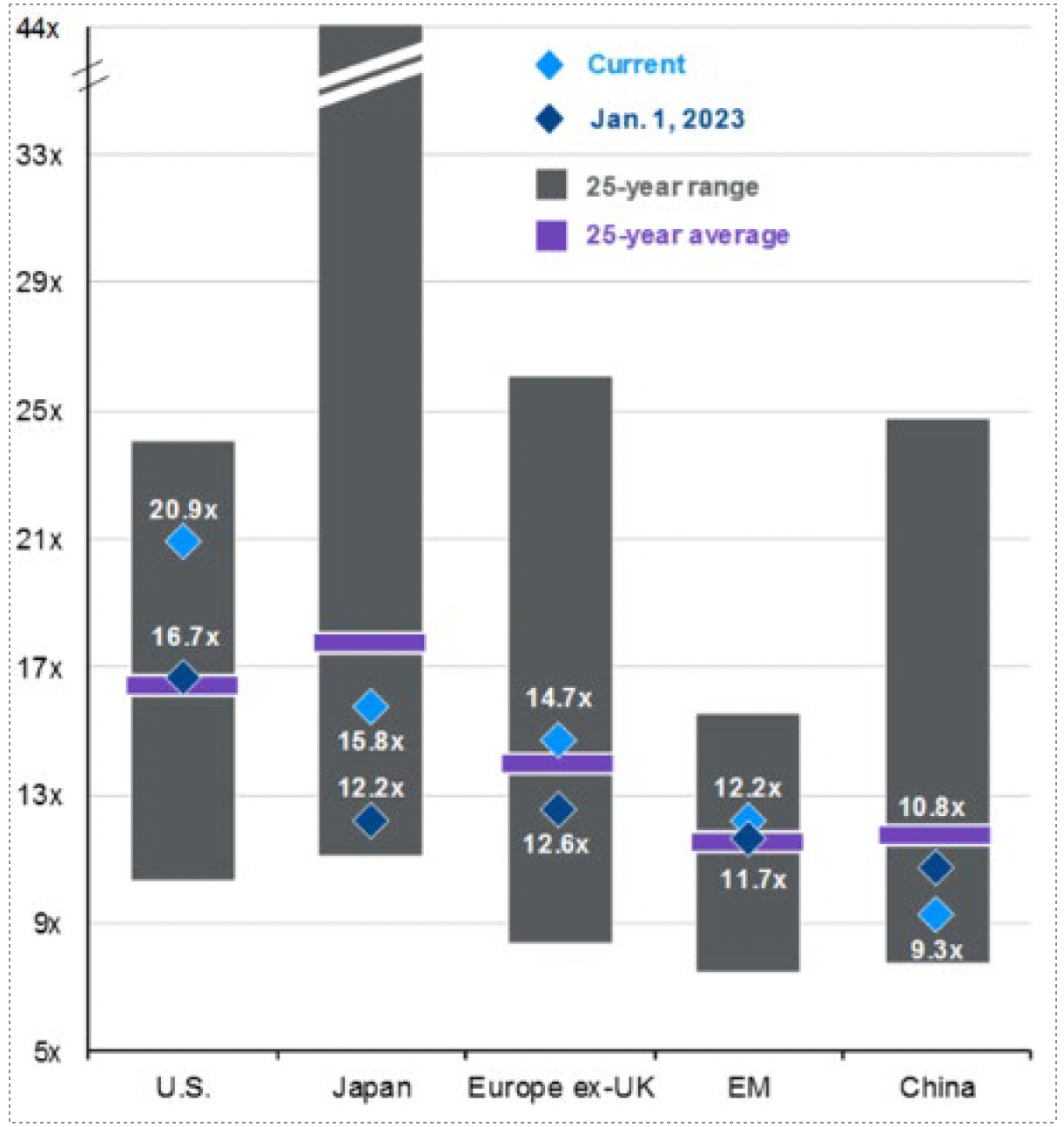

Source: JPMorgan Chase Guide to the Markets

International markets have been strong, even with headwinds through the strengthening in the U.S. Dollar. We continue to see strong opportunities in both international developed markets and emerging markets as those economies appear to be further along in the business cycle than we are, which may lead to a period of relative outperformance. Though geopolitical tensions are continuing to flare up, we believe that any sort of interest rate cuts would be highly supportive for international and emerging markets and overshadow some of the geopolitical uncertainty. From a valuation perspective, there continues to be a strong case for ex-US equities being attractive relative to domestic equities. The secular themes playing out with near-shoring and friend-shoring occurring in many emerging markets continue to create a compelling thesis for an allocation to those markets.

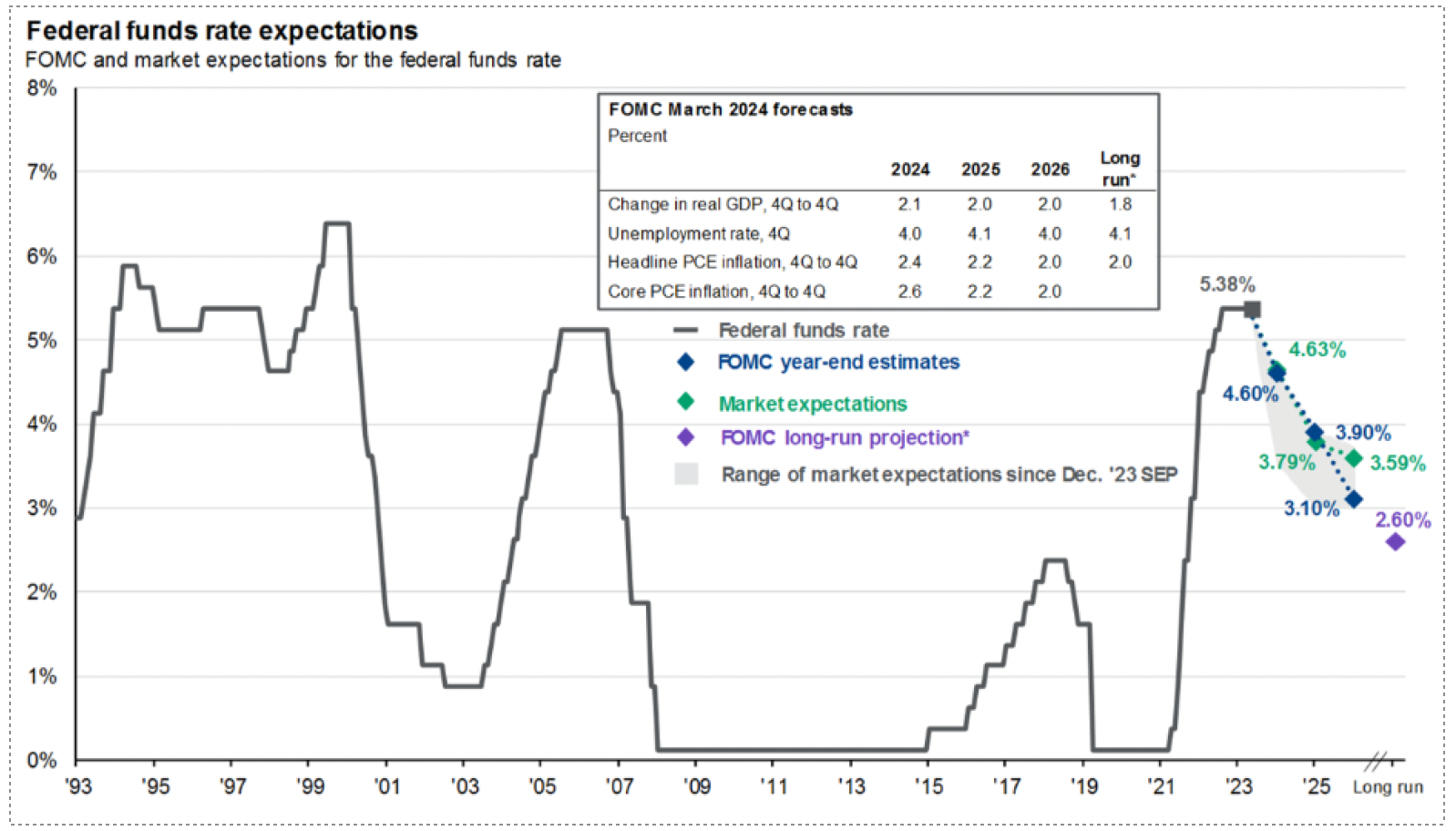

Fixed Income’s Year to Shine

The markets and the Fed are both communicating rate cuts in some capacity this year as inflation continues its slow trudge downward. The headwinds that the Fed was previously communicating appear to be receding, which will give them more flexibility over the coming quarters with rates. Though the Fed is a neutral body, we see politicization rising with an election year becoming a driving factor as to where rates may go. Fed Chair Jerome Powell does not want a recession and would like to tout a soft landing, whereas President Joe Biden doesn’t want a recession in Source: JPMorgan Chase Guide to the Markets an election year and point to a win for U.S. consumers. As a result, there will likely be pressure exerted from political forces that exist. We continue to foresee 1 or 2 rate cuts to a total of 1.00%. These cuts would keep conditions modestly tight to exert pressure on inflation but would ease pressure on both the consumer and the interest payments being made by the U.S. Government.

Source: JPMorgan Chase Guide to the Markets

Holistically, we see fixed income performing well through the remainder of 2024 driven mostly by higher yields and tight credit spreads relative to Treasuries. Global bonds denominated in U.S. dollar may continue to be choppy as the U.S. dollar has continued to strengthen through the year, though local-currency denominated bonds may fare well.

Summary

As domestic markets have pushed higher, the concentration of the top constituents has continued to be narrow with overall muted earnings growth. The economic backdrop remains mixed globally with further signs of potential slowdowns. Fixed income continues to be attractive from a total return perspective as the potential for rate cuts loom on the horizon.

We look forward to working with individuals and businesses throughout the year in navigating markets, financial planning, and taxes. As we like to remind our clients, time in the market is always more important than timing the market. Volatility is common in markets and, though it can make some uneasy, it is important to stick to a long-term plan. If you have any questions, please don’t hesitate to reach out to our team.